North Africa's Digital Health Moment, and the Gap That Decides It

Growth is not adoption. The scaling gap is the test.

The money and the infrastructure are arriving in MENA digital health. Whether the products arrive with them is a separate question, and it is the one that matters.

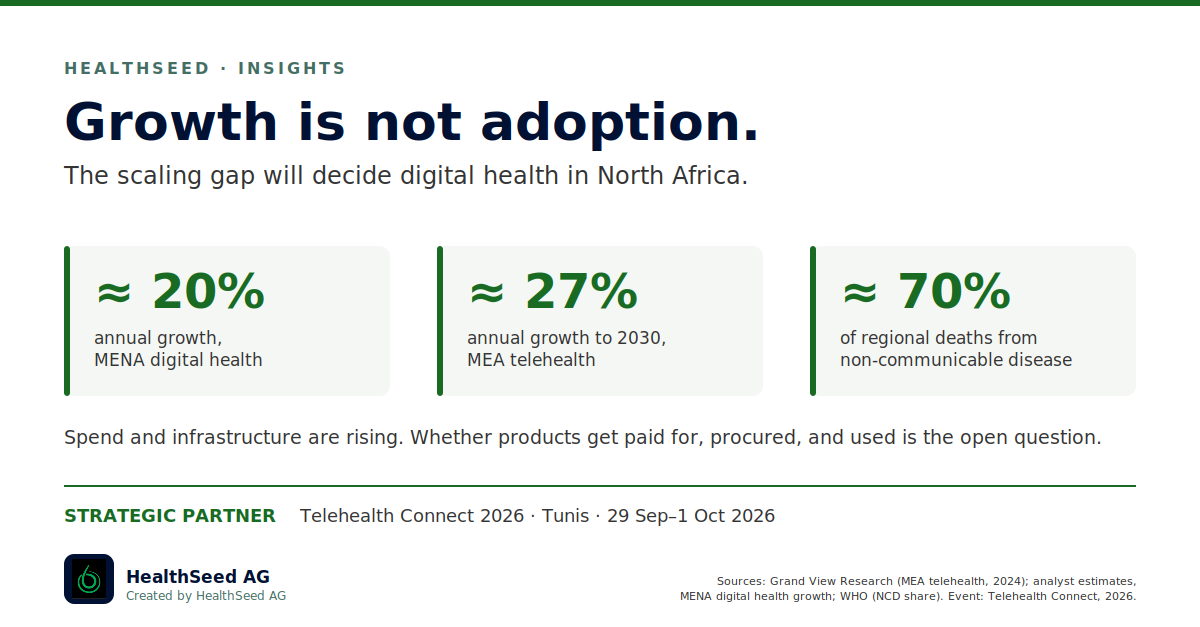

The headline numbers are real. Digital health across the Middle East and North Africa is growing at close to 20% a year on most analyst estimates, and the Middle East and Africa telehealth segment alone was valued at around USD 4.5 billion in 2024, on a path of roughly 27% annual growth to 2030 (Grand View Research). Non-communicable diseases account for about 70% of deaths in the region (WHO), which sustains demand for the remote monitoring, AI diagnostics, and connected-care models that digital health promises. National strategies in Saudi Arabia, the UAE, Egypt, and across North Africa pull in the same direction, and regulators from Saudi Arabia's SFDA to Egypt's EDA have spent 2025 and 2026 making device and digital health pathways clearer and more predictable.

None of that guarantees adoption. Growth in spend and infrastructure is a different thing from a health system that pays for a product, procures it, integrates it into a clinical workflow, and keeps using it. That distance, between a validated product and durable use inside a system, is what we call the scaling gap. It is where most health innovations stall, and it is more visible in MENA than the growth figures suggest.

Where products meet systems

The gap shows up in specific, unglamorous places. Reimbursement is the first: who pays, on what evidence, at what price, and whether a private-pay model can carry a product until a public payer engages. Regulation is the second, since the authority, the classification, and the timeline differ by market, and a route cleared in one country rarely transfers cleanly to the next. Then there is procurement, the question of how a hospital or a ministry actually buys and who has to say yes. Data governance has become its own commercial question, because in a region writing its rules in real time the handling of patient data is something buyers probe early. And almost nothing moves without local partners: the distributor, the clinical champion, or the system integrator who opens a door a foreign product cannot open alone.

I have spent two decades on the system side of these questions, launching specialty and oncology products across several countries and, in one case, leading a legislative reimbursement change that opened patient access across multiple products and indications. The lesson repeats across markets. The science earns the right to compete. The commercial and regulatory architecture decides whether anyone benefits from it.

Why MENA, and why now

The region is not a single market, and that is part of the difficulty. A product that works in Dubai's private system meets different payers, procurement, and price references in Cairo, Riyadh, or Tunis. Fragmentation raises the cost of every market entry and rewards companies that sequence deliberately rather than chase the whole region at once. The underlying demand is structural: young populations, rising chronic disease, governments treating digital infrastructure as a national priority, and a growing base of local founders who understand their own systems better than any outsider can.

The summit's focus on cybersecurity and health data governance is not incidental. In a region setting its data rules in real time, how patient information is stored, moved, and protected is one of the first questions a serious buyer asks, and one of the most common reasons a deal stalls. For founders, treating data protection and security as a commercial capability rather than a compliance cost is increasingly what separates the companies that close institutional contracts from the ones that pilot indefinitely.

Much of our work helps companies move between markets, including from the US into Europe, where the same gap between a cleared product and a paying system catches founders who assumed clinical validation was the hard part. North Africa and MENA add another set of systems to that map. For some founders the region is a primary market; for others it complements a European entry, or benefits from European evidence and partnerships. Either way, the sequencing decision, which market first and on what evidence, is worth as much as the product roadmap.

Why Tunisia

Tunisia sits at an interesting point in this picture. The country has a deep pool of engineers, researchers, and clinicians recognised internationally, and a young base of telemedicine and digital health startups beginning to find their footing. Its national strategy is explicit about positioning Tunisia as a regional reference for health innovation, bridging Europe and Africa, and the government has put real weight behind that ambition.

What HealthSeed is doing in Tunis

That is why we have joined Telehealth Connect 2026 in Tunis as a strategic partner. The summit runs from 29 September to 1 October 2026, under the High Patronage of the President of the Republic of Tunisia and with the Tunisian Ministry of Health closely involved, with an agenda spanning telemedicine, AI in healthcare, cybersecurity, and health data governance.

Our role is hands-on. As part of the programme, we will work directly with founders in the Health Tech Startup Bootcamp on the disciplines that decide whether a venture scales: sharpening the value proposition for a specific payer and provider, mapping the market access and regulatory route market by market, building the investment readiness that turns a pilot into a fundable company, and structuring the partnerships that make international expansion possible. These are the points where good products usually stall, and they are the work we do.

What this means

The growth figures will keep climbing, and capital will keep finding the region. The companies that benefit will be the ones that treat market access, reimbursement, and partnership as the product problem they are, early, rather than as something to fix after the pilot. The disciplines that determine whether a health venture reaches patients are consistent whether the market is Tunis, Berlin, or Boston. The systems differ; the points where companies get stuck repeat. Our work is to help founders cross that gap wherever they are building, and North Africa is a place where that work is needed now.

If you are building, investing, or partnering in the region and will be in Tunis, we would value the conversation.